Wednesday, August 23, 2006

Are they Lying or just Victims of Mass Hysteria?

I bought my house in 2004 and had to suck up to a 6.25% mortgage because I nailed the a temporary peak - Timing is everything.

The amazing thing is I could refinance if I wanted to. Although with my mortgage being paid off in 12 years, I don't think it's worth paying the appraisal fee.

I do find it fascinating at how right Greenspan was when he told people that an adjustable rate mortgage makes sense for many people. The press was outrage. And they lashed out at him as he raised interests rates.

But maybe Greenspan understood what I told you folks back in the beginning of the year. John Doe consumer , especially after the revised bankruptcy laws is a far better credit risk than any business a bank could loan it's money to.

We are see how the shifting of the bank perspective on who is a better credit risk is flooding the supply of money available for the consumer to borrow.

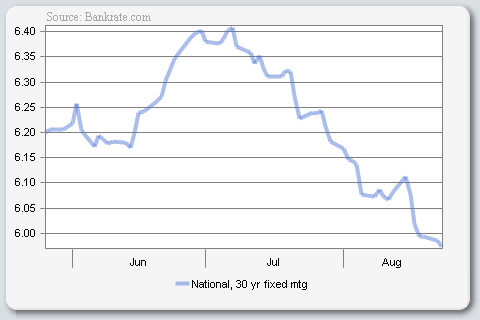

Rates are dropping, not rising.

What is even more fascinating by this, is the refusal for the media to acknowledge the drop in mortgage rates. Your average person believes mortgage rates are climbing and that the time to buy a house has pass. The truth is it is now easier than ever to qualify for a mortgage and they are cheap.

SO WHAT HAPPENS WHEN RATES ARE AT A TWELVE MONTH LOW? The day is coming.

Comments:

<< Home

You sure are fixated on the 30 year fixed rate. Check out the short term rates YoY, the bubble areas arent dominated by 30 yr fixed, they were dominated by neg option ARMs and IO loans. Now that the short term rates have gone up so much those marginal buyers (which were the majority of buyers) cant buy.

It doesnt matter that we are historically low interest rates compared to history. All that matters is that we are at "historic" highs relative to the last 2 years.

Lax lending standards and cheap money is the reason why the nation went insane on real estate. Now we are in an overbought condition, with higher rates, and lending standards tightening (just wait for the Fed guidance for some real fun). If the economy slows, it'll be a bloodbath, otherwise it'll just be stagnant for many years while wages catch up to fundamentals.

It doesnt matter that we are historically low interest rates compared to history. All that matters is that we are at "historic" highs relative to the last 2 years.

Lax lending standards and cheap money is the reason why the nation went insane on real estate. Now we are in an overbought condition, with higher rates, and lending standards tightening (just wait for the Fed guidance for some real fun). If the economy slows, it'll be a bloodbath, otherwise it'll just be stagnant for many years while wages catch up to fundamentals.

# posted by  : 8/24/2006 3:08 AM

: 8/24/2006 3:08 AM

: 8/24/2006 3:08 AM

You sure are fixated on the 30 year fixed rate. Check out the short term rates YoY, the bubble areas arent dominated by 30 yr fixed, they were dominated by neg option ARMs and IO loans.

People that bought arms in the past can now refiance with 10, 12, 15, and 30 year mortgages. By buying the arm and refiancing with a fix rate mortgage the facts are the facts. They did save money. You cannot argue with the truth.

Arms were not for everyone. Some folks work in occupations where they must seek new work every few years. If you know this applies to you you run the risk of a change in credit rating at the time refinacing the debt is required. Only if your credit rating has change did you get burn buying arms when Greenspan recomended them.

Now we are in an overbought condition, with higher rates, and lending standards tightening (just wait for the Fed guidance for some real fun).

Aboulutly false regarding higher interst rats and tightening ending standards. I believeyo are victim of mas hysteria

Post a Comment

People that bought arms in the past can now refiance with 10, 12, 15, and 30 year mortgages. By buying the arm and refiancing with a fix rate mortgage the facts are the facts. They did save money. You cannot argue with the truth.

Arms were not for everyone. Some folks work in occupations where they must seek new work every few years. If you know this applies to you you run the risk of a change in credit rating at the time refinacing the debt is required. Only if your credit rating has change did you get burn buying arms when Greenspan recomended them.

Now we are in an overbought condition, with higher rates, and lending standards tightening (just wait for the Fed guidance for some real fun).

Aboulutly false regarding higher interst rats and tightening ending standards. I believeyo are victim of mas hysteria

Subscribe to Post Comments [Atom]

<< Home

![]()

Subscribe to Posts [Atom]