Tuesday, November 22, 2005

The Wizard of OZ

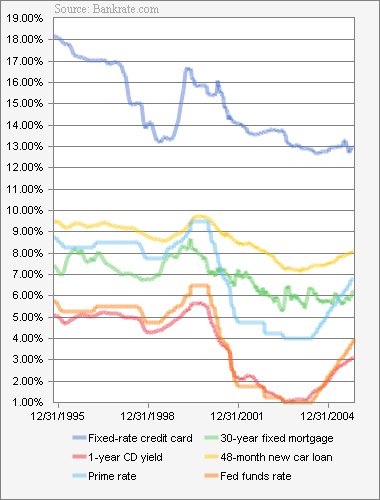

We all been told that the above chart is how it works. The Fed raises or lowers the interest rates by changing the intra bank loan rate. BUT IS THAT TRUE?

Here are the Fed rates for 2005 compared to mortgage rates

Jan 2.25----5.80

Feb 2.50----5.72

Mar 2.75----6.01

Apr 2.75----6.02

May 3.00----5.87

Jun 3.25----5.77

Jul 3.25----5.84

Aug 3.50----6.00

Sep 3.75----5.94

Oct 3.75----6.21

So what is going on? From March 2005 to September 2005 the Fed rate went up over 36% while mortgage rates went down over 1%.

The answer is simple economics. Banks got screw big time by World Comm, Global Crossing, Enron, US Airways. With each bankruptcy that wiped these companies debt obligation away the banks lost big. We hear a lot of talk about personal bankruptcy, but the hard cold facts are a business will wash away debt in a second. While the individual won't out of shame. On top of that personal bankruptcy laws were revised to make it harder on the individuals to wipe away debt.

so if you were a bank with a finite number of billions to loan out. Would you rather see most of that money go to John Doe with the confidence you will see it come back, or to the New Global Crossing, MCI, a Airline, and so on?

Though the Fed is raising interests rates we are seeing a shift in comfort level by the banks as to who is more reliable with debt. This growing shift will keep mortgage rates low.

![]()

Subscribe to Posts [Atom]